Money stress has a way of making people feel disqualified before they even apply for help. A lower income can make borrowing feel intimidating, especially when so much financial advice online assumes everyone has perfect credit, steady savings, and room in their budget for emergencies. Real life rarely looks that clean. Millions of Americans are balancing rising costs, inconsistent income, existing debt, or financial setbacks while still trying to stay afloat responsibly.

That is exactly why more borrowers are exploring low income installment loans. A low income installment loan gives borrowers access to funds that are repaid through scheduled payments over time, rather than requiring full repayment all at once. More importantly, many lenders evaluate far more than income alone when reviewing applications.

At FlexMoney, the focus is helping borrowers understand how qualification actually works so they can make informed financial decisions with more clarity and less panic.

What You’ll Learn

- Low income does not automatically disqualify borrowers from installment loans

- Many lenders focus more on stable recurring income than a specific salary amount

- Credit score matters, but it is only one part of the approval process

- Pre approval systems using soft credit checks help borrowers compare options safely

- Installment loans often provide more manageable repayment timelines than payday loans

- Responsible borrowing starts with understanding loan terms, fees, and repayment expectations

Why Installment Loans Feel Less Overwhelming Than Payday Loans

Financial emergencies rarely arrive at convenient times. A car repair, overdue utility bill, unexpected medical expense, or sudden drop in income can quickly create pressure that feels impossible to manage with one paycheck alone. For many borrowers, the problem is not simply needing money. The problem is needing enough breathing room to recover financially without making the situation worse.

That is where installment loans often feel more manageable. Unlike payday loans that usually require repayment within weeks, installment loans break repayment into scheduled payments over a longer period of time. Borrowers know exactly what they owe and when payments are due, which creates more predictability during stressful situations.

According to the Consumer Financial Protection Bureau, payday loans often require repayment within a very short timeframe, which can make financial recovery more difficult for some borrowers.

Many lenders now offer more flexible installment loan options designed for borrowers with varying financial backgrounds, including people with lower income, limited credit history, or inconsistent work schedules.

That flexibility does not remove responsibility from borrowing. It simply reflects the reality that financial situations are rarely one size fits all.

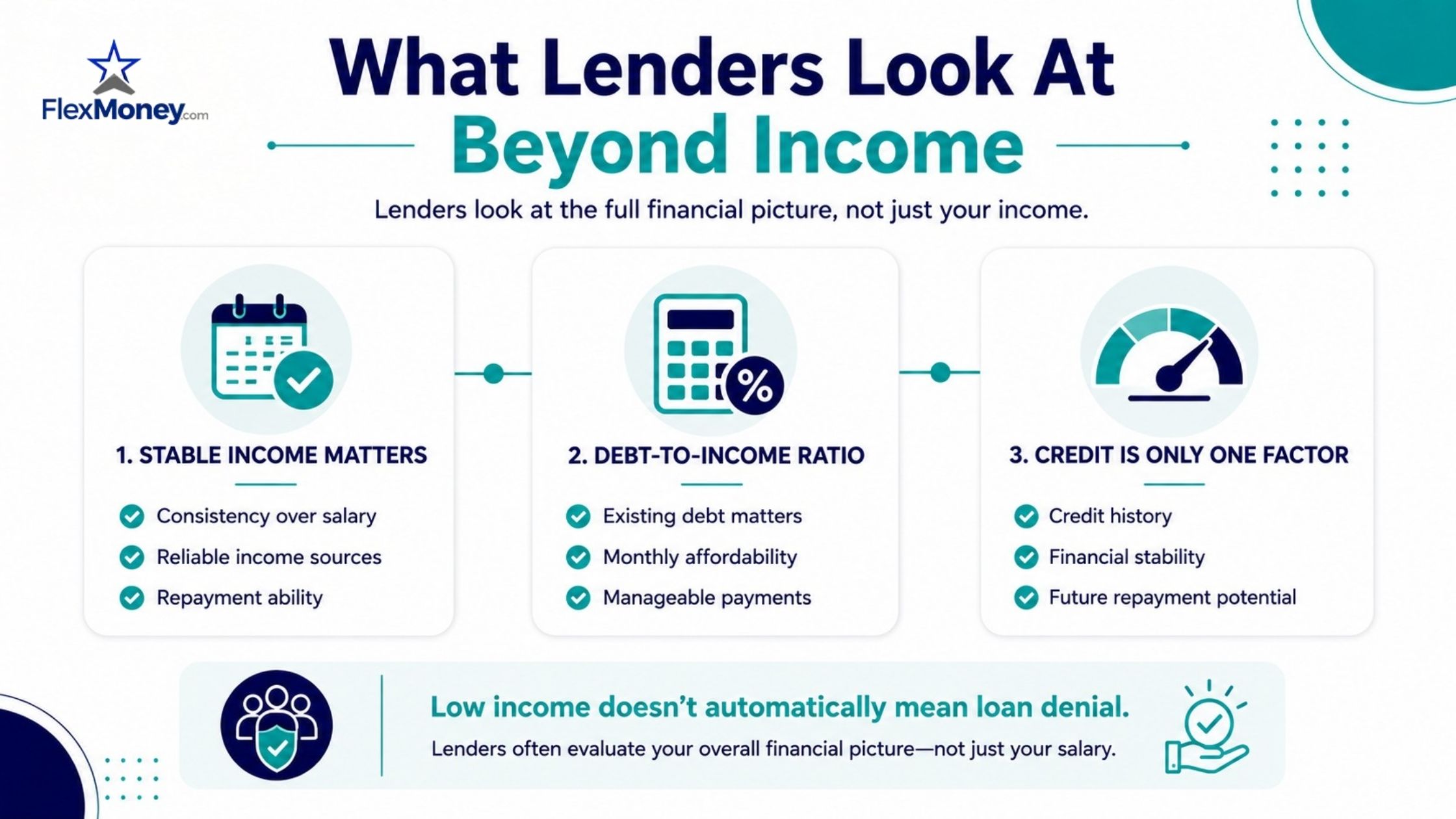

What Lenders Actually Look At Beyond Income

One of the biggest misconceptions about low income installment loans is the belief that lenders only care about how much money someone earns.

Income matters, but lenders usually evaluate several financial factors together.

Consistent Income Often Matters More Than High Income

Many lenders care less about whether someone earns a large salary and more about whether their income appears steady and reliable.

A borrower with modest but consistent recurring income may appear less risky than someone earning more money inconsistently.

Recurring income can include:

- Full time employment

- Part time work

- Self employment income

- Gig economy earnings

- Pension payments

- Disability benefits

- Child support or alimony

- Government assistance income

The primary concern for lenders is whether scheduled loan payments realistically fit within a borrower’s financial situation.

Consistent repayment habits may also influence how installment loans may affect credit over time. Making payments on schedule can help build positive payment history, while missed payments or repeated late payments may negatively impact a borrower’s credit profile.

Debt to Income Ratio Helps Lenders Assess Risk

Lenders also evaluate existing financial obligations through a debt to income ratio, commonly called DTI.

This compares how much debt a borrower already pays monthly against how much they earn. A borrower may still qualify with existing debt, but lenders want reassurance that additional payments will remain manageable.

Experian notes that debt to income ratio is one of the most common tools lenders use to assess whether monthly loan payments are manageable for borrowers.

Even borrowers completing online installment loan applications are commonly reviewed through some form of debt assessment.

Can You Qualify With Bad Credit?

Bad credit can absolutely make borrowing more difficult, but it does not automatically eliminate every option.

Many lenders understand that credit challenges happen for countless reasons, including medical emergencies, job loss, divorce, or periods of financial instability.

Some installment lenders work specifically with borrowers who have:

- Lower credit scores

- Limited borrowing history

- Previous late payments

- Collections accounts

- Financial hardship history

What lenders often care about most is whether repayment appears realistic moving forward. That is why borrowers should avoid assuming rejection before even exploring available options.

Why Soft Credit Checks Matter When Comparing Loans

Borrowers under financial pressure often apply to multiple lenders quickly out of desperation. That approach can sometimes create additional problems.

Some lenders perform hard credit inquiries immediately during the application process. Too many hard inquiries within a short period may lower credit scores and create concern for future lenders reviewing the borrower’s financial activity.

Pre approval systems using soft credit checks are generally safer for comparison shopping. Soft inquiries allow lenders to review general financial information without negatively affecting credit scores. Borrowers can compare loan terms, payment structures, and approval likelihood more carefully before committing.

This gives applicants more control when deciding whether to apply for online loans responsibly.

Understanding Loan Terms Before You Accept Funds

Approval alone should never be the only goal. Borrowers should understand exactly how repayment works before accepting any loan agreement.

Interest Rates Can Vary Widely

Installment loan rates depend on several factors, including:

- Credit profile

- Income stability

- Loan amount

- Repayment timeline

- State regulations

- Overall lending risk

Borrowers with stronger financial profiles may qualify for lower rates, while higher risk applications may receive more expensive offers.

Some Lenders Charge Additional Fees

Not every lender structures loans the same way.

Some lenders may charge:

- Origination fees

- Late payment fees

- Returned payment fees

- Early repayment penalties

Responsible lenders should clearly explain all fees upfront rather than hiding them within confusing contract language. Transparency matters, especially for borrowers already managing tight budgets.

What Information Do Most Installment Lenders Require?

Modern lending has become significantly faster than traditional bank borrowing, especially with digital platforms.

Still, lenders generally require basic verification information before approving a loan.

Identity Verification Requirements

Borrowers are commonly asked for:

- Full legal name

- Residential address

- Phone number

- Active email address

- Government issued identification

- Social Security Number or ITIN

Income Verification Requirements

Some lenders still request traditional documents like pay stubs or employer letters. Others now rely on secure digital systems that verify recurring deposits directly through connected bank accounts. This process often speeds up approvals while reducing paperwork for borrowers seeking personal loans online.

How Borrowers Can Improve Their Approval Chances

Borrowers do not need perfect finances to strengthen an application. Even small improvements can sometimes help lenders feel more confident approving a loan.

Review Your Credit Report Before Applying

Errors on credit reports are more common than many borrowers realize. Incorrect balances, outdated accounts, or duplicate collections can negatively affect approval odds unnecessarily.

Checking reports beforehand gives borrowers the opportunity to correct issues early. The Federal Trade Commission also recommends reviewing your credit reports regularly to catch potential errors that could affect loan applications. Federal Trade Commission free credit reports resource.

Borrowers can also access free federally authorized credit reports through AnnualCreditReport.com before applying for financing.

Lower Existing Debt If Possible

Reducing monthly obligations may improve debt to income ratios and make repayment appear more manageable. Even small improvements can positively influence approval decisions.

Avoid Excessive Applications

Submitting too many applications too quickly can create additional financial strain and unnecessary credit inquiries. Researching lenders carefully before applying is often the smarter approach.

Alternatives to Installment Loans Worth Considering

Installment loans are not always the right solution for every financial situation.Sometimes alternative options may reduce financial pressure without creating additional debt.

Possible alternatives could include:

- Payment arrangements with creditors

- Utility hardship programs

- Employer paycheck advances

- Credit counseling services

- Credit union emergency loan programs

- Community assistance programs

- Borrowing from trusted family members

Even for borrowers who ultimately decide to move forward with financing, understanding online loan requirements ahead of time can help reduce confusion, avoid unnecessary applications, and improve the chances of finding a loan that realistically fits their financial situation.

Responsible borrowing starts with understanding all available options rather than rushing into the first approval opportunity available.

Why Customer Support Still Matters With Online Lending

Fast funding and digital convenience matter, but customer support still plays a major role in responsible lending.

Borrowers should be able to:

- Access their loan information easily

- Understand repayment expectations clearly

- Receive transparent answers about fees or payments

- Easily speak with customer support if questions or payment concerns arise during the loan process

A lender should never feel impossible to reach once funds are deposited. Strong customer support helps borrowers feel more confident throughout the borrowing process, especially during stressful financial periods.

Key Takeaways

- Low income alone does not automatically prevent installment loan approval

- Many lenders focus more on stable recurring income than salary size

- Soft credit checks help borrowers compare lenders more safely

- Installment loans often provide longer repayment timelines than payday loans

- Understanding fees, rates, and repayment expectations is essential before borrowing

- Responsible borrowing starts with realistic repayment planning

Frequently Asked Questions

Can you get an installment loan with a low income?

Yes, many lenders consider factors beyond income alone. Stable recurring income, manageable debt levels, banking activity, and repayment ability may all influence approval decisions. Some lenders specifically work with borrowers who have lower income or nontraditional earnings, although loan terms and approval amounts vary by lender.

What income do you need to qualify for an installment loan?

Most lenders do not publish one fixed minimum income requirement. Instead, lenders often evaluate consistency of income and whether repayment appears manageable alongside existing financial obligations. Recurring deposits from employment, benefits, or self employment income may help strengthen a borrower’s application.

Do installment loans hurt your credit score?

An installment loan itself does not automatically hurt credit. Making payments on time may help build positive payment history over time. However, missed payments, repeated hard credit inquiries, or borrowing beyond your financial capacity can negatively affect credit and overall financial health.

Are installment loans better than payday loans?

For many borrowers, installment loans provide more manageable repayment structures than payday loans. Installment loans generally offer longer repayment periods and predictable payment schedules, while payday loans often require full repayment within a very short timeframe. Borrowers should still review rates, fees, and repayment obligations carefully before borrowing.

How quickly can online installment loans be approved?

Approval timelines vary depending on the lender and verification process. Some online lenders provide decisions within minutes and may release funds within one business day after verification and digital contract signing. Traditional lenders using manual documentation processes may take longer to complete approvals and funding.

The Bottom Line on Low Income Installment Loan Qualification

A lower income does not automatically mean rejection. Many lenders now evaluate borrowers more holistically by considering recurring income, banking activity, existing debt, repayment ability, and overall financial stability rather than focusing only on salary size.

That flexibility helps explain why more borrowers are exploring flex pay installment loans online instead of relying on short term borrowing options with intense repayment pressure.

The Consumer Financial Protection Bureau also provides educational resources on borrower protections and high cost lending practices to help consumers make informed financial decisions.

At FlexMoney, the process is designed to feel straightforward, transparent, and approachable. Borrowers can explore loan options, understand repayment expectations clearly, and complete the process entirely online without unnecessary complications.

The goal is never simply approval. The goal is finding a borrowing solution that realistically fits your financial situation without creating additional stress later.